B2B businesses are thriving, gaining billion-dollar valuations and seeing blockbuster listing. Can the good times last?

If you ask us, Icarus wasted his time sticking wax onto feathers. He should have simply moved to India, built a logistics app (since he was looking for a mobility solution) and waited for demonetisation and Goods and Services Tax (GST) rollout. Wait, what? These disruptive changes brought many sectors and companies crashing to the ground! Yes, that is true. But they also gave wing to many B2B start-ups. Udaan became a unicorn in the shortest time, in three years since its founding. A handful of other start-ups, including Rivigo and Delhivery, too, got billion-dollar valuations. In June 2019, IndiaMART, which runs a marketplace for businesses, saw an impressive listing — 21% premium over its issue price of  973. Within three months, its price doubled and today, its market cap is at $0.8 billion. Internet firms rarely see such success on the trading floor. The company, founded in 1996 by Dinesh Agarwal as an exports marketplace, made a clever pivot to the domestic market in 2008. Today, the listing platform has more than 130,000 suppliers. “In the early 2000s, China began to dominate international trade, which directly impacted Indian exports. At the same time, domestic consumption started to grow. That’s when I decided to change our market focus,” says Agarwal. Of course, this two-decade-old company is a bit long in the tooth to be a start-up, but its success is illustrative of the optimism around the B2B segment in India.

973. Within three months, its price doubled and today, its market cap is at $0.8 billion. Internet firms rarely see such success on the trading floor. The company, founded in 1996 by Dinesh Agarwal as an exports marketplace, made a clever pivot to the domestic market in 2008. Today, the listing platform has more than 130,000 suppliers. “In the early 2000s, China began to dominate international trade, which directly impacted Indian exports. At the same time, domestic consumption started to grow. That’s when I decided to change our market focus,” says Agarwal. Of course, this two-decade-old company is a bit long in the tooth to be a start-up, but its success is illustrative of the optimism around the B2B segment in India.

Show me the money

These start-ups largely serve small and medium businesses (SMBs) in the country, and a recent report by Zinnov says that these businesses will have nearly 7x the money to invest in about five years. India is home to around 75 million SMBs — accounting for nearly 40% of the nation’s GDP — and generate 180 million jobs currently. The report estimates that they will spend around $14-16 billion on productivity, communication, discoverability and payments solutions in 2019 and this figure will rise to $105 billion by 2024 as the SMB base expands. It pegs the SMB digitisation opportunity alone at around $80 billion over the next five years. No wonder that there is a huge spurt in the number of start-ups addressing this opportunity.

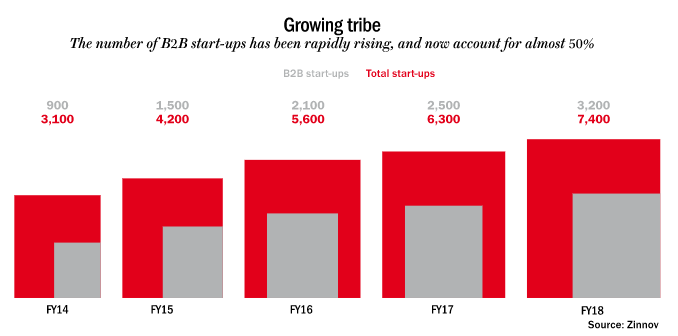

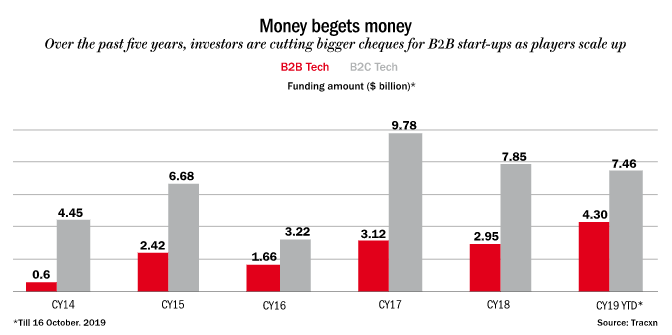

While B2B start-ups constituted 900 of the total 3,100 in 2014, the number increased to 3,200 in 2018, which was 43% of the total start-ups in India (See: Growing tribe). Investors including Tiger Global, Sequoia, Accel, Lightspeed and Nexus Venture Partners, have moved in quickly as well. According to Tracxn, the overall funding increased from $600 million in 2014 to $4.3 billion in 2019 (See: Money begets money).

The good times began in 2016 with Reliance Jio’s cheap data plans, which brought nearly everyone from your fifth-generation grocer to the first-generation electronics-store owner online. Smartphones became affordable too. Then, the note ban (affectionately called ‘de-mon’) forced smaller businesses to adapt to digital payments (or perish) and finally, in 2017, GST brought order in this disorganised sector. It not only improved the ease of transporting goods across the country but also improved the overall transparency levels.

“GST was definitely an accelerator because what was a state-driven infrastructure has now become pan-India,” says Rahul Garg, founder and CEO, Moglix. The firm, which began operations in 2015, has built an e-commerce platform that caters to about 500,000 SMEs across 45 product categories, and has raised around $100 million from investors including Tiger Global, Sequoia India and Accel India. WhatsApp and Facebook had become verbs by then, and Flipkart and Amazon were as familiar as the neighbourhood store. “But many didn’t think it was possible to sell steel, plastics and polymer online,” says R Narayan, founder and CEO, Power2SME, a company founded in 2012 that helps SMEs across construction, manufacturing and engineering sectors to reduce procurement costs. It clocked revenue of 10 billion in FY19 and has raised $60 million in funding,

Narayan says that manufacturers initially refused to work with them. “They would connect us with a distributor and say let’s do this as an experiment and see how it goes. It was only after we built volume that they began to see the value proposition of working with us and having an online presence,” he says.

However, B2B also has an advantage over customer-facing companies. For one, there is loyalty. “It is not easy to find your first customer,” says Rajesh Yabaji, CEO, BlackBuck, “but once you do, they tend to stick around for at least a year or two.” His company, founded in 2015 and valued at $950 million, provides logistics services through a trucking platform. He connects shippers with available truckers and also facilitates payments. “The decision by shippers to stay on the platform is based more on consistent user experience, and not just on initial discounts or pricing,” he adds. He should know, since BlackBuck has over 300,000 truck owners on its platform and counts Asian Paints, Coca-Cola, ITC, Tata Steel and Hindustan Unilever among its clients.

The Indian B2B e-commerce space is estimated to grow to $700 billion by 2020, which is more than twice of what it was in 2014 at $300 billion. But in a fragmented market with inflexible retailers, converting an offline B2B model into an online one can stir up a hornet’s nest. In India, procurement and distribution of industrial goods have been done manually for decades. This has led to a fragmented supplier base, which leaves little scope for inventory optimisation. Besides that, this rickety network is ridden with middlemen, namely wholesalers and distributors. This broken supply chain is one of the biggest problems the B2B start-ups are fixing. “We built the entire supply chain infrastructure and industrial clusters around them,” says Garg. These young companies run platforms on which brands and retailers can sell and buy products, to ensure better margins for both. Apart from that, they also manage the collection of goods from suppliers, storage in warehouse and last-mile delivery to customers.

That’s not all though. By providing working capital or tying up with third-party lenders such as NBFCs or other fintech companies, they also take care of their clients’ credit cycle. For instance, a small business can now get loans at an interest rate of 12-15%, as compared to 30-35% from traditional moneylenders. “Earlier, the distributor was providing credit and supply chain capabilities, and both didn’t have economies of scale. Each of them would only look at a network of about 500 shops. But with the entry of formalised players, their networks can manage tens of thousands of shop owners or small businesses,” says Sameer Brij Verma, managing director, Nexus Venture Partners. “As networks grow larger, credit will decouple. And we can already see this happening,” adds Verma.

Built to scale

Sabka Vikas then, but then how do the B2B start-ups make money? Some of them charge per transaction and others levy a fixed subscription fee. The founders of Udaan are taking a leaf out of their former employer Flipkart’s playbook and funding their aggressive growth through VC money. The poster child of this booming trend provides end-to-end services — from logistics to credit — besides giving access to its trading platform. Incorporated in June 2016 by three former Flipkart executives Amod Malviya, Sujeet Kumar and Vaibhav Gupta, the start-up has expanded its operations to 900 cities, connecting three million retailers and 20,000 sellers. In just three years, the firm has raised $870 million from marquee investors such as Tencent, GGV Capital, DST Global and Lightspeed Ventures. In its last round, it raised $585 million, which bumped up its valuation to $2.3 billion.

Udaan uses free services as the customer acquisition model. The co-founders believe that once enough small businesses experience higher revenue growth through the platform, they would eventually be willing to share a part of that revenue. That’s why, for now, it is reliant on its credit business for revenue than its marketplace business despite clocking an annual GMV of $2 billion. In FY19, the company spent 3.63 billion, almost 5x more than it did in FY18 to earn revenue of 250 million. More than 50% of it came from lending activities. At the other end, IndiaMART, which charges a subscription fee of 3,000/month or 30,000/year, clocked FY19 annual revenue of 5 billion with an operating profit of 800 million. In fact, it also posted a profit of 200 million.

Making money as a horizontal player in the B2B space isn’t as easy as it is in the consumer space. “In case of B2C e-commerce, the same customer on Flipkart or Amazon will buy a phone, apparels and even electronics, but in B2B, a customer who buys steel is unlikely to go for plastics,” says Nexus Venture Partners’ Verma. While Udaan services businesses across various categories including home appliances, apparels and staples, Ninjacart from the same city runs a platform that helps retailers and merchants source fruits and vegetables directly from farmers. This means better prices for 45,000 farmers, and reliable supply and efficient sourcing for 70,000 kirana stores. The start-up collects and distributes fresh produce through its network of fulfillment centres, which are stocked based on demand. “The biggest problem is perishability. So, we stay closer to the market and have been doing that from day one. It also helps us understand how the market works,” says Thirukumaran Nagarajan, CEO, Ninjacart. The story goes that two of the start-up’s founders would go to Kalasipalyam market (Bengaluru’s main fruit and vegetable market) in the wee hours to observe how prices are fixed and the way trade is done.

Those were the initial days of learning. Today, the start-up relies heavily on technology, right from setting the purchase price, and how the crates should be sorted and packed, to running its logistics network. It makes the whole process more efficient, of course, but the best part is that the start-up is able to assure payment within 24 hours to its farmer-partners, who had to earlier wait for weeks. “The customer is happy, the farmer is happy. The only real challenge is adding more hubs and training people day in and day out,” adds Nagarajan and says that they are also looking at adjacent categories to expand into, using the network they have built. Analysts believe this could mean non-perishables such as FMCG.

These young entrepreneurs make the whole process, of converting an offline model into an online one, look easy. It may seem like a simple two-step process — observe and digitise. But don’t be fooled. It takes a lot of patience and much negotiation to change business behaviour. Ashish Jhina, co-founder and COO of another B2B start-up Jumbotail, founded in 2015, also in the Garden City, says, “Initially, shopkeepers would ask us if we could take orders on the phone, since they would have exhausted their data pack. We would insist on app-only orders and recharge their phones, the cost of which would be added to the bill.” Jumbotail is a well established start-up in the FMCG space, serving 20,000 kirana stores in Bengaluru and a few in Hyderabad. These retail stores form the backbone of India’s $600-billion grocery and FMCG business, while modern trade (department stores, supermarkets and hypermarkets) makes up only for 10% of the overall market. Small neighbourhood stores make up for the rest.

According to Jhina, both demand and supply for food and groceries are highly fragmented, and the start-up began by aggregating demand. Using its platform, retailers can pick from 3,500 SKUs and Jumbotail promises delivery within 24-48 hours through its network of fulfillment centers. It has also tied up with third-party lenders to provide working capital for buyers, and the start-up determines their credit-worthiness through their transactional data. “We realised that providing pricing information and a platform for buyers and sellers is not enough. We have to assure our buyers timely delivery and the seller, timely payment. Traditional intermediaries have been doing this for years, but it is difficult to scale up beyond a point when you do things manually. You cannot scale up without technology,” says Jhina. The company, which is close to clocking $100 million in sales, makes its money by charging a commission to sellers and providing credit to buyers and running promotions for brands. The initial resistance from retailers and suppliers to move online gradually faded and Jumbotail’s founders say the entire procurement process has now become paperless.

Amit Sharma, founder of ShopX also swears by technology. His start-up, founded in 2015, too, has hitched its wagon to small-format stores. With the start-up’s digital catalogue, retailers in Tier-II and Tier-III towns can order directly from big brands such as HUL and P&G. ShopX also handles logistics with third-party partners, who use its proprietary technology, allowing ShopX to track the movement of goods. “You cannot solve a problem with deep discounting or by having a large fleet. We are present in 23 states and our entire sales and marketing engine is almost completely digitised,” he says. Within four years of its founding, the start-up has won the trust of over 100,000 retailers, who are connected to 100 brands. According to Sharma, ShopX’s retailers have seen their fill rates improve from 70% to 99%. The start-up makes 14-16% margin from the sellers for distribution and marketing, part of which is shared with retailers. The company is currently clocking GMV of $800 million and is also looking at other markets such as Indonesia, Vietnam and a few African countries in the next two to three years. “Just like India, general trade in these markets is also very fragmented,” says Sharma.

Hello, disruption

Even as investors continue to pump money into B2Bs and some of them are not even thinking much about generating revenue, forget profit, the sector’s biggest challenge could from Mukesh Ambani-led Reliance Industries. After changing the landscape of the Indian telecom industry, the conglomerate is looking to enter the B2B ecommerce space. As a first step, its retail initiative JioMart launched its services to online shoppers in Navi Mumbai, Thane and Kalyan. The venture will also partner with local grocers and equip them with point of sales terminals, low-interest working capital, inventory management skills, and help with GST compliance, all of which many of the B2B start-ups are solving in parts. If the financial muscle of Reliance Industries can shake biggies such as Vodafone-Idea, many B2B start-ups will also end up as casualties once Reliance starts to expand its footprint.

As many of the B2B start-ups brace for the entry of Reliance Industries, a handful of them are finding niches and building a business model around them. KhataBook has digitised the very Indian khata system of informal lending and borrowing. The start-up, founded in 2018, even takes its name from it. Its mobile app helps small business owners track money owed to them with a digital ledger, and sends reminders when payments are due through SMS and WhatsApp messages. “The lending mechanism is a problem that affects every business irrespective of the category they are in, and that’s why we decided to solve it,” says Ravish Naresh, CEO, KhataBook. Since many merchants are first-time internet users, Naresh says that the UI and user experience needed to be extremely simple. In addition to that, KhataBook supports 11 local languages including Hindi, Gujarati, Tamil and Telugu.

“Instead of making the app text-heavy, we have made a lot of our FAQs video-centric and offer regional language options as well,” he says. With over three million merchants using the app and recording over $3 billion in transactions, the company is yet to charge its users. The idea is to create a dense network of suppliers and retailers. “You know what they are buying, the frequency of their purchases and their payment track record. Once you have enough data, there are all sorts of services you can offer to the members on the network,” says Dev Khare, partner, Lightspeed Ventures, which has invested in OkCredit, a competitor of KhataBook. Over the next 12-18 months, KhataBook plans to offer credit and other financial services to its users. “They have never had a paper or digital trail and hence, the banks have ignored them. This makes the entire banking suite an untapped avenue for us,” says Naresh. Since the company already has transaction details of the users, it will also be quicker to grant loans. Having raised $29 million from GGV Capital, DST Global and Sequoia, the start-up will also foray into e-commerce, software services and legal services.

Future-ready

Just as Udaan, B2B start-ups such as KhataBook and OkCredit aren’t losing sleep over monetisation just yet. They believe they will be able to build a revenue layer by offering credit services. Seems like a no-brainer but the catch is, a whole host of fintech firms are already courting cash-strapped SMEs and these B2B start-ups will either have to apply for an NBFC license or tie-up with existing banks and NBFCs for capital. The NBFC crisis has already shown how fickle surplus capital can be. In fact, as India deals with an economic slowdown, SMEs are the worst hit in terms of demand and their receivables stuck, as large companies delay payments. SMEs will have to stay liquid and long enough for these start-ups to charge them. Hence, those relying on a future transaction-based model will need their investors to write more fat cheques.

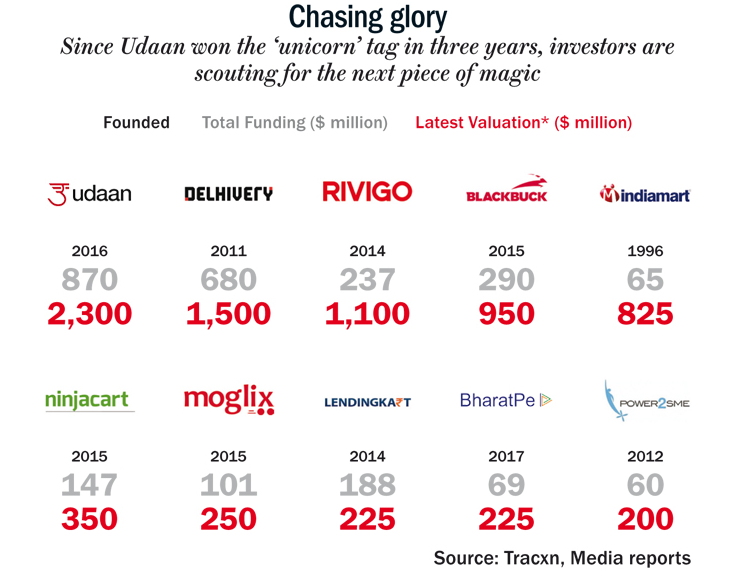

Thankfully, the financers seem happy to oblige. They are betting on the fact that India has more than 100 million farmers, 15 million small manufacturers and 30 million traders and retailers, and only a fraction of them have been covered by e-commerce so far. But Nexus’ Verma warns that the transition will not be an easy one. “The supply chain in India is broken and inefficient. You cannot digitise these existing inefficiencies and expect them to become efficient. You have to reorient the supply chain,” he says. While the revenue model of many B2B start-ups is yet to be put to the test, investors seem willing to back their scaling up plans generously, like they did with B2C start-ups (See: Chasing glory). You can see that from the valuation they have assigned Udaan, despite its modest revenue stream. It is nearly 3x what they have assigned the 20-year-old IndiaMART. All the signs point out that their optimism is reminiscent of the euphoria around B2C start-ups that led to mindboggling valuations. Yes for Flipkart, Walmart did come to its rescue and Amazon India has deep pockets to keep it going for a long time. But in the B2B space, while the market opportunity is large enough, a similar outcome might not play out. Weaker players may go out of business but much of the growth will have to be organic, and relying on investors’ cheques alone may not be a prudent strategy. So, while they soak in all the love and remain the flavour of the season, all players must also keep in mind the perils of flying too close to the sun with a hack.